By Jeffrey Barnett, Founder and Managing Principal, Fintegrity® LLC

April 2026

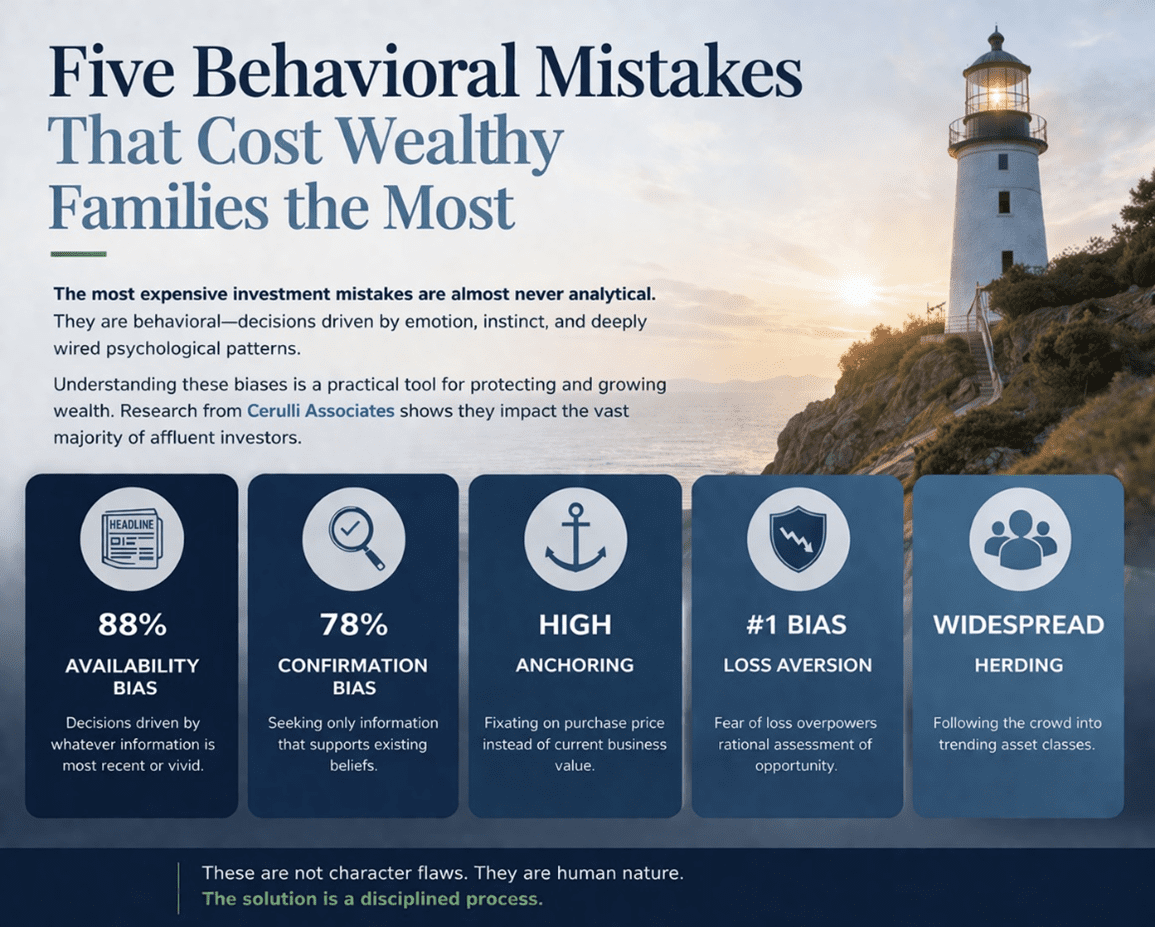

The most expensive investment mistakes I see are almost never analytical. They are not the result of picking the wrong stock, misreading an earnings report, or failing to predict a recession. They are behavioral — decisions driven by emotion, instinct, and deeply wired psychological patterns that even the most intelligent and successful people struggle to override.

This is not a theoretical observation. Behavioral finance — the study of how human psychology affects financial decision-making — is the foundation of how I manage portfolios at Fintegrity®. Understanding these patterns is not an academic exercise. It is a practical tool for protecting and growing wealth.

According to research from Cerulli Associates, the overwhelming majority of affluent investors exhibit behavioral biases that directly affect their investment outcomes. What follows are the five I encounter most frequently among the high-net-worth families I work with — each illustrated with a composite example drawn from the kinds of situations that arise in the $2 million to $25 million range.

1. Availability Bias: Letting Headlines Drive Your Portfolio

Prevalence: 88% of affluent investors, according to Cerulli Associates — the most common behavioral bias in the data.

Availability bias is the tendency to make decisions based on whatever information is most easily recalled — typically the most recent or most vivid. In investing, this means the last headline you read, the last market commentary you heard, or the most dramatic story in the news cycle carries disproportionate weight in your thinking.

What it looks like in practice: A client reads a series of articles about commercial real estate distress. The reporting is accurate — certain segments of the Commercial Real Estate (CRE) market are indeed under pressure. Based on this information, which is vivid, recent, and available, the client wants to eliminate all real estate exposure from the portfolio. The problem is that their exposure is to residential REITs and industrial logistics properties, which are performing well. The availability of negative CRE headlines has overridden the relevance of those headlines to their actual holdings.

Why it is costly: Availability bias causes investors to overweight recent information and underweight base rates and long-term data. It is the mechanism behind much of the reactive selling that destroys wealth during downturns. The headline is vivid and frightening, so it feels like it should drive a portfolio decision, even when it should not.

2. Anchoring: The Inherited Stock You Cannot Sell

Prevalence: High across all wealth levels, and particularly pronounced among investors who have held positions for years, per Cerulli.

Anchoring is the tendency to fixate on a reference number — usually the price at which you bought a stock, or the price at which it peaked — and use that number as the basis for decisions about the current position, regardless of whether that number is relevant today.

What it looks like in practice: A family inherited a significant position in a blue-chip company when a parent passed away. The stock was worth $120 per share at the time of the step-up in basis. Over the next three years, the company’s competitive position deteriorated — margins compressed, a product line failed, and the stock drifted to $85. The family resisted selling because the stock “used to be at $120” and they were waiting for it to “come back.” That $120 was their anchor. But the business had changed. The relevant question was not whether the stock would return to $120 but whether the business at $85 represented a better use of that capital than other opportunities. It did not. By the time they agreed to sell, the stock was at $62.

Why it is costly: Anchoring causes investors to hold losing positions far too long and to sell winning positions too early. The purchase price is irrelevant to the investment decision today. What matters is the current valuation relative to the business’s current and future earning power. An anchor prevents you from asking the right question: “If I did not already own this, would I buy it today at this price?”

3. Loss Aversion: The Panic Sell That Costs a Fortune

Prevalence: Ranked the #1 emotional bias affecting client decision-making in Cerulli’s survey of over 300 financial advisors.

Loss aversion is one of the most powerful forces in human psychology. Research by Daniel Kahneman and Amos Tversky, the founders of modern behavioral economics, demonstrated that the pain of losing a dollar is roughly twice as intense as the pleasure of gaining one. When it comes to investing, this means that during a downturn, the emotional pressure to “stop the bleeding” can easily overwhelm a rational assessment of whether selling is the right decision.

What it looks like in practice: In early 2020, a family with a $4 million portfolio watched the S&P 500 fall 34% in 23 trading days. They experienced market declines before but never felt anything this fast or this severe. The combination of a global pandemic, daily headlines about economic shutdown, and a portfolio that was suddenly showing a $1.3 million loss triggered a decision to move to cash “until things calm down.” By the time they felt calm enough to reinvest — four months later — the market had already recovered most of the decline. The family permanently lost roughly $600,000 of the rebound by sitting in cash during the fastest recovery in market history.

Why it is costly: Loss aversion is expensive because it is asymmetric. The decision to sell feels urgent — the pain is happening right now. But the decision to reinvest always feels premature — things never feel “calm enough.” The result is a pattern where investors sell low and buy back high, or worse, never reinvest at all. The DALBAR Quantitative Analysis of Investor Behavior has documented a persistent 3% to 4% annual gap between what the market returns and what the average investor earns, driven overwhelmingly by this pattern.

4. Overconfidence in Concentrated Positions: The One Stock That Is “Different”

Prevalence: Especially pronounced among entrepreneurs, executives, and families whose wealth was built through a single company or industry.

Overconfidence bias in investing manifests as the belief that the position you know best is the position that deserves the most capital. For executives who built their career at a company, or entrepreneurs who sold a business in a particular industry, this creates a dangerous concentration of risk in what feels like the area of greatest expertise.

What it looks like in practice: An executive retired from a pharmaceutical company with $8 million in net worth, of which $5.2 million was concentrated in the company’s stock. His reasoning was straightforward: “I know this company better than any analyst on Wall Street. I understand the pipeline, the competitive dynamics, and the management team.” He was right about all of that. What he did not predict was a patent cliff that reduced the company’s revenue by 40% over 18 months, a regulatory action that delayed two key drug approvals, and a CEO departure that triggered a further sell-off. His position lost 55% of its value. The institutional knowledge he had was genuine but incomplete — it did not account for the events that no insider can foresee. According to Morgan Stanley, 85% of individual stocks experience a larger decline than the overall index, and nearly 40% of stocks that suffer a 50% peak-to-trough drop never fully recover.

Why it is costly: Concentration risk compounds because the same event that damages the stock often damages the investor’s other income sources simultaneously. The executive whose wealth is tied to a single company’s stock may also lose their job, their unvested options, and their industry network in the same downturn. Diversification is not a sign of lacking conviction. It is a recognition that even the best-informed investor cannot predict every outcome for a single company.

5. Herding: The Country Club Portfolio

Prevalence: Widespread, and particularly pronounced in social settings where investment choices become a form of status signaling.

Herding bias is the tendency to follow the crowd — to invest in whatever asset class, strategy, or theme is generating the most conversation. Among high-net-worth individuals, this often manifests as pressure to allocate to the same alternative investments that peers are discussing at social gatherings, board meetings, or professional events.

What it looks like in practice: Over dinner with friends, a couple learned that several families in their social circle had allocated 25% to 30% of their portfolios to private equity and venture capital funds. The conversation made their own portfolio — which was generating strong returns through a diversified mix of individual stocks and bonds — feel unsophisticated. However, upon examining the specific funds their friends were invested in, the picture was less compelling than the dinner conversation suggested: high fees (2% management plus 20% of profits), 10-year lock-up periods with no liquidity, and historical returns that, after fees, roughly matched those of publicly traded small-cap value stocks — without the illiquidity. The desire to invest was not driven by analysis. It was driven by the social discomfort of being the only family at the table without an allocation to alternatives.

Why it is costly: Herding leads to allocation decisions that do not reflect the investor’s actual financial plan, risk tolerance, or liquidity needs. It also tends to be pro-cyclical — by the time an asset class is popular enough to dominate social conversation, much of the return has already been captured. The families who allocated to private equity at the peak of the cycle in 2021 are now navigating an environment where many of those positions are marked down and the capital is locked up for years. As economist Robert Shiller has documented, “infectious narratives” about wealth and prestige can drive investment decisions just as powerfully as fundamentals — and often in the wrong direction.

What All Five Biases Have in Common

Each of these biases exploits the gap between what feels right and what is right. They are not signs of poor judgment or lack of intelligence. In fact, some of the most successful people I work with are the most susceptible — because the same confidence, decisiveness, and pattern recognition that built their wealth can work against them in markets that do not reward those instincts the same way.

The solution is not to eliminate emotion from investing. That is impossible. The solution is to have a disciplined process that makes the important decisions before the emotions arrive — and an advisor who will hold the line on that process when human nature says to abandon it.

That is what behavioral finance means in practice. Not a theory. A guardrail.

Jeffrey Barnett is the founder and Managing Principal of Fintegrity LLC, a registered investment adviser based in Tenafly, New Jersey. Fintegrity’s investment approach is grounded in behavioral finance, managing portfolios for high-net-worth families nationwide using individual stocks and bonds. For more information, contact Jeff@Fintegrity.com or 201-266-6829.

Fintegrity is registered with the New Jersey Bureau of Securities. This article is for informational purposes only and does not constitute investment advice. The examples above are composite illustrations for educational purposes and do not represent any specific client. Past performance is not indicative of future results. All investments involve risk, including possible loss of principal.