Health Savings Accounts (HSAs) have become an increasingly popular tool for individuals and families to save for future medical expenses while reaping significant tax benefits. Understanding the contribution limits, eligibility rules, and the tax advantages associated with HSAs can make a meaningful difference in your overall financial plan.

What Is a Health Savings Account?

A Health Savings Account is a type of savings account that allows you to set aside money on a pre-tax basis to pay for qualified medical expenses.

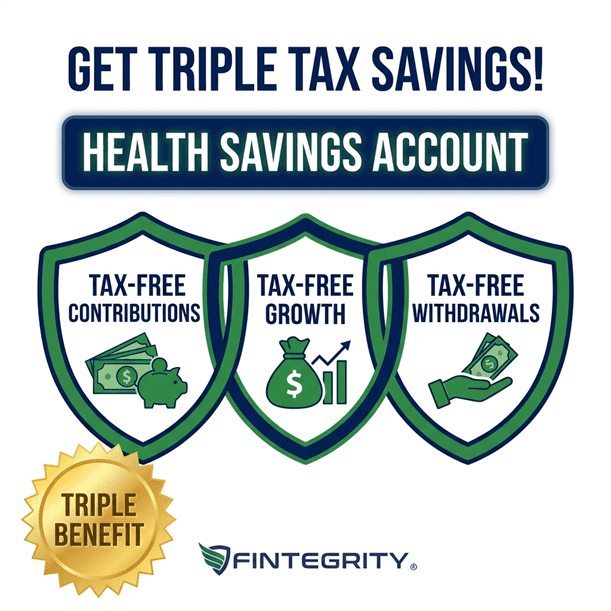

Triple Tax Savings

Health Savings Accounts provide three ways to save on taxes, even for those who do not itemize their deductions on their federal income tax returns.

- Tax-Free Contributions: HSA contributions are pre-tax (or tax-deductible if you contribute post-tax dollars, even if you do not itemize your deductions).

- Tax-Free Growth: Interest or other capital gains earned on the funds in your HSA are not subject to federal (and in most cases, state) taxes.

- Tax-Free Withdrawals: HSA spending for qualified medical expenses is tax-free, regardless of when you make them.

When choosing your health plan each year, consider the tax benefits of HSA-eligible plans in calculating which plan best meets your needs.

HSA Contribution Limits

Each year, the IRS sets limits on how much you can contribute to your HSA. For 2026, the contribution limits are:

- Individual Coverage: $4,400

- Family Coverage: $8,750

If you are 55 or older, you can contribute an additional $1,000 as a catch-up contribution.

These figures may change each tax year, so check current rules and limits.

HSA Eligibility

To be eligible to contribute to an HSA, you must be enrolled in a High-Deductible Health Plan (HDHP). For 2026, this means your health plan has:

- An annual deductible of at least $1,700 for individual coverage and $3,400 for family coverage.

- An out-of-pocket maximum that does not exceed $8,500 for individual coverage and $17,000 for family coverage.

Not all health plans with high deductibles are HSA-eligible. To be HSA-eligible, a plan must not offer any benefit beyond preventive care before meeting the annual deductible.

And to contribute to an HSA you must:

- Not be claimed as a dependent on someone else’s tax return

- Not be enrolled in Medicare

Medicare Beneficiaries

Once you enroll in Medicare, you can no longer contribute to a Health Savings Account. However, you can still use the money already in your HSA after you enroll in Medicare to help pay for medical expenses tax-free, including out-of-pocket Medicare costs, deductibles, copayments, and coinsurance.

You should stop contributing to your HSA at least six months before applying for Social Security benefits or Medicare, because Social Security benefits are typically retroactive and you could be penalized for HSA contributions made during that period.

HSA Contribution Deadline

You generally have until the tax filing deadline to contribute to an HSA. For tax year 2026, you can make contributions until April 15, 2027.

HSA Providers

Employer benefit plans often offer an HSA as an option on plan menus. However, many brokerage firms offer these accounts independently from a workplace. I recommend Fidelity Investments’ HSA because it has no fees and a good selection of investment choices.

HSA investments should be chosen based on the time horizon of when you might spend the money. Spending that could be needed within a couple of years should be maintained in a money market fund. Longer-term spending will likely grow the most in a diversified portfolio of stocks, but will have large variability in annual returns. Investing in stocks always carries risks and it is important to understand these risks before deciding on your investment strategy.

Maximizing Your HSA Tax Benefit

If you use your HSA to cover current medical expenses, you gain the benefit of making tax-free withdrawals. However, you will be missing tax-free growth.

Paying current medical expenses out of pocket allows your HSA to remain invested for the long term, growing tax-free over time. Later, when you have substantial growth in the account or are in retirement (when you are likely to have higher healthcare costs), you can then make tax-free withdrawals for medical expenses.

In addition, after you reach the age of 65, you can make withdrawals from your HSA for non-medical expenses without penalty. However, these withdrawals will be taxed as income like a traditional IRA.

HSA Tax Penalties

While HSAs offer valuable tax benefits, they can also come with tax penalties if you contribute too much each year or use the money to pay for ineligible expenses.

If you exceed the annual maximum contribution limit, you may face a 6% excise tax on your excess contributions in the year you overcontributed and failed to remove the excess contribution and its earnings. The excess contribution is also considered taxable income. If you correct the error before the tax filing deadline for the year, you may be able to avoid income tax and the excise tax for that year.

If you use HSA dollars for ineligible expenses, you will be charged a steep tax penalty. If you do so under the age of 65, you will have to pay a 20% penalty plus any applicable income taxes on what you withdraw. If you are 65 or older, you can use HSA money for ineligible expenses penalty free, though you will have to pay income taxes.

Conclusion

Because of the triple tax benefit, maximizing contributions to an HSA each year should be prioritized ahead of IRA contributions.

This article is for informational purposes only and does not constitute tax or investment advice. Consult a qualified tax professional regarding your specific situation. Fintegrity LLC is a registered investment adviser regulated by the New Jersey Bureau of Securities.