By Jeffrey Barnett, Founder and Managing Principal, Fintegrity® LLC

April 2026

Every January, Wall Street’s top strategists publish their predictions for the year ahead. Where will the S&P 500 finish? Will there be a recession? Which sectors will lead?

Every January, they are wrong.

According to research compiled by Avantis Investors, the median Wall Street strategist forecast misses the actual S&P 500 return by an average of nearly 19 percentage points (2018–2025). In 2024, the S&P 500 rose 23%. The most optimistic major forecast called for 13%. JPMorgan’s strategists predicted an 8% decline. The range of outcomes tells you everything you need to know about the predictive value of these exercises.

When evaluating an investment manager, focus less on their market predictions and more on their strategy, which should remain consistent regardless of market behavior.

The Forecast Problem

The appeal of a forecast is obvious. It offers certainty in an uncertain world. “The market will go up 10% next year” is a concrete, actionable statement. It feels like information.

But it is not information. It is a guess dressed in a spreadsheet. Markets are driven by an unknowable combination of earnings, interest rates, geopolitical events, consumer sentiment, regulatory changes, technological disruption, and the collective emotional responses of millions of participants. No model accounts for all of these variables, and no human can reliably predict how they will interact.

The issue isn’t a lack of competence among forecasters; many are brilliant analysts with deep expertise. The problem is that the task itself is impossible. Short-term market movements are inherently unpredictable, a fact demonstrated so consistently across decades of data that basing investment decisions on forecasts is a behavioral error in itself. It’s an overconfidence bias that the financial industry has a strong incentive to encourage.

What an Investment Philosophy Actually Is

An investment philosophy is something fundamentally different from a forecast. It is not a prediction about what will happen. It is a framework for deciding what to do under any set of conditions.

At Fintegrity®, our philosophy is grounded in behavioral finance — the recognition that markets are not always rational and that investor psychology creates persistent opportunities for disciplined managers. This means:

- We focus on what companies are worth, not where their stock prices are headed. Our research is centered on business fundamentals — earnings power, competitive position, balance sheet strength, management quality. We buy ownership stakes in individual businesses we understand, at prices we believe understate their long-term value.

- We accept that we cannot predict short-term market movements — and we do not try. Instead, ee construct portfolios designed for long-term performance across various market environments, a fundamentally different approach than attempting to predict short-term market fluctuations.

- We recognize that our clients’ greatest risk is often their own emotional response to volatility. The most expensive investment mistakes are almost never analytical. These behaviors involve selling when fear overtakes discipline or chasing a hot sector because everyone else seems to be making money there.

A philosophy answers the question: “When the next crisis hits and markets fall 20%, what will you do?” A forecast simply guesses when that crisis might arrive.

The Measurable Cost of Reacting to Forecasts

This is not an abstract argument. The cost of abandoning a disciplined philosophy in favor of reactive decision-making has been quantified repeatedly.

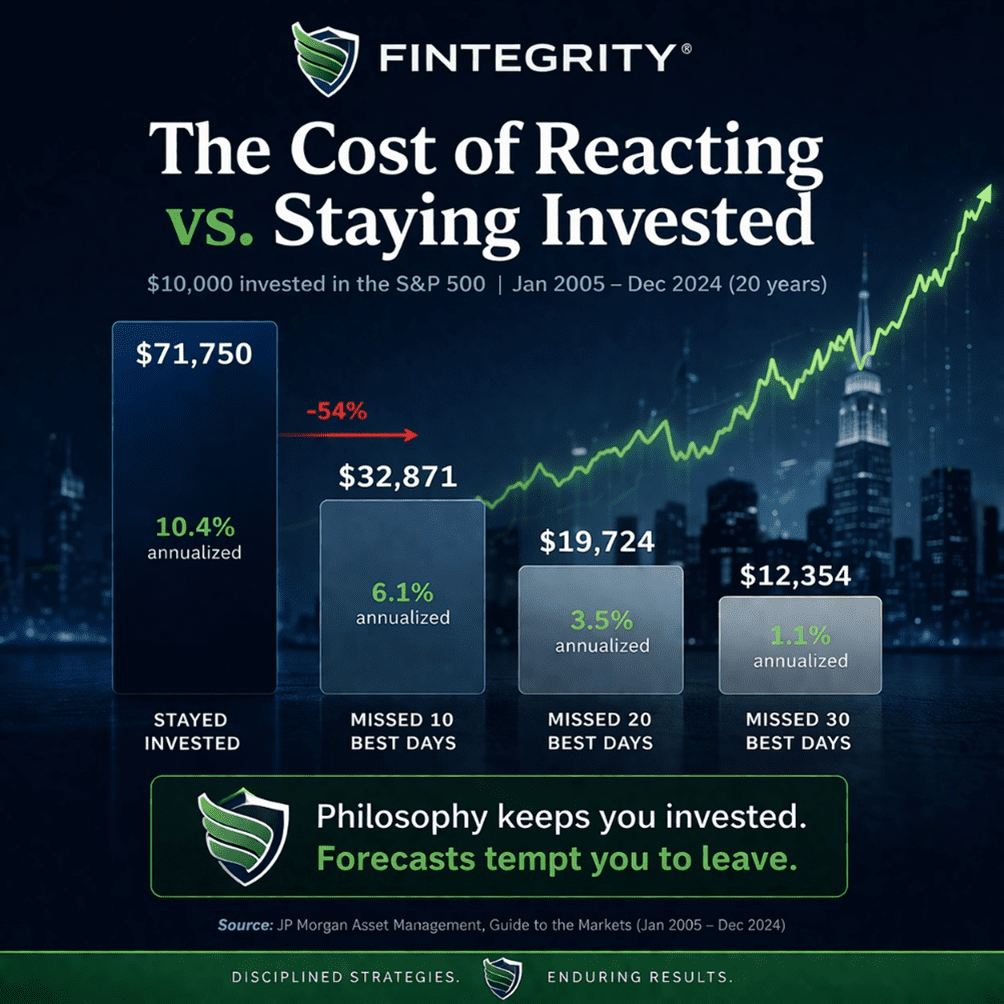

JP Morgan Asset Management published research showing that a $10,000 investment in the S&P 500 from January 2005 through December 2024 would have grown to $71,750 — a 10.4% annualized return. But if that same investor, spooked by a forecast or a headline, moved to cash and missed just the 10 best trading days during that 20-year period, the result would have been $32,871 — a 54% reduction. Missing the 30 best days would have left the investor with $12,354, barely above the original investment after two decades.

Here is what makes this data particularly relevant: seven of the 10 best market days during this period occurred within two weeks of the 10 worst market days. The days when the market surges — the days you must be present for — happen right after the days when every instinct says to run. The investor who exits the market after a bad week, waiting for things to “calm down,” almost always misses the recovery that follows.

The annual DALBAR Quantitative Analysis of Investor Behavior reinforces this pattern. Over the 30-year period from 1992 to 2021, the average equity fund investor earned 7.13% annually, while the S&P 500 returned 10.65%. That 3.5% annual gap — the “behavior gap” — was not caused by picking the wrong funds. It was caused by buying and selling at the wrong times, driven by emotional responses to short-term market movements.

On a $1 million portfolio over 20 years, a 3.5% annual behavior gap is the difference between roughly $7.4 million and $3.9 million. That is $3.5 million lost — not to bad markets, but to bad timing driven by the belief that someone, somewhere, can tell you what the market will do next.

What Philosophy Looks Like in Practice

A sound investment philosophy is not passive. It does not mean buying an index fund and ignoring your portfolio. It means having a clear, repeatable process for making investment decisions that does not depend on predicting the unpredictable.

At Fintegrity, this translates into specific practices:

- Individual stock and bond selection. Unlike other advisors, I avoid packaged products like mutual funds or third-party model portfolios. Instead, I personally research and evaluate every business before including it in your portfolio, ensuring each holding is tailored to your specific allocation. This conviction is crucial during market downturns, as it allows us to confidently hold what we understand.

- Tax-aware decision-making. Philosophy extends to how we manage the after-tax return, not just the pre-tax return. Harvesting losses during downturns, managing the timing of gains, and structuring portfolios with tax efficiency in mind are all expressions of a disciplined framework rather than reactions to forecasts.

- Proactive rebalancing. When market dislocations occur—such as energy stocks surging while technology stocks decline, or interest rate changes altering the relative value of fixed income—a guiding framework dictates our response. We trim positions that have become overweight and allocate to those that are now undervalued. This approach is the antithesis of chasing performance; it requires the conviction that a disciplined process, while sometimes uncomfortable, will prove effective over time.

- Clear communication during volatility. When clients call during a downturn, they do not reach a call center or a junior associate reading from a script. They reach the person who built their portfolio and can explain exactly what we own, why we own it, and what we are doing about the current environment. That conversation, grounded in philosophy rather than panic, is often the most valuable service an advisor provides.

How to Evaluate a Manager’s Philosophy

When you are interviewing prospective advisors, consider asking these questions:

“What is your investment philosophy?” The answer should be specific, consistent, and expressed in the manager’s own words — not a recitation of marketing language. If the answer amounts to “we diversify across asset classes based on your risk tolerance,” that is a process description, not a philosophy.

“What did you do during the last major downturn?” This reveals whether the philosophy is real or decorative. An advisor who claims to be disciplined and long-term oriented but moved clients to cash in March 2020 did not have a philosophy. They had a preference that they abandoned under pressure.

“How do you make buy and sell decisions?” Look for a repeatable framework. At Fintegrity, every investment decision runs through a consistent analytical process: business quality, competitive position, valuation, and portfolio fit. That process does not change based on whether the market had a good week or a bad one.

“What will you do if the market drops 25% next month?” The right answer is not “I will call you to discuss.” The right answer describes a specific set of actions — rebalancing, harvesting losses, identifying opportunities — that the advisor would take based on the portfolio’s design, not based on a prediction about what comes next.

The Advisor’s Real Job

The financial industry has spent decades cultivating the idea that the advisor’s value is in knowing what the market will do. It is a compelling narrative, and it sells. But it is not true.

The advisor’s real job is to build a framework that works regardless of what the market does — and to hold the line on that framework when human nature says to abandon it. That is what a philosophy does. It replaces the question “What will happen?” with the question “What should we do?” And the answer to that second question should not change every time a headline does.

Your wealth was not built by following forecasts. It should not be managed by following them either.

Jeffrey Barnett is the founder and Managing Principal of Fintegrity LLC, a registered investment adviser based in Tenafly, New Jersey. Fintegrity manages portfolios for high-net-worth families nationwide using individual stocks and bonds, grounded in behavioral finance principles. For more information, contact Jeff@Fintegrity.com or 201-266-6829.

Fintegrity is registered with the New Jersey Bureau of Securities. This article is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. All investments involve risk, including possible loss of principal.