By Jeffrey Barnett, Founder and Managing Principal, Fintegrity® LLC

April 2026

You met with a senior partner. The conversation was impressive — deep knowledge, confident perspective, genuine interest in your situation. You signed. Three months later, you realize the person managing your portfolio is someone you have never met.

If this sounds familiar, you are not alone. It is the most common experience in wealth management, and it is one of the most costly, not because the junior associate is incompetent, but because the structure itself creates problems that compound over time.

How the Handoff Works

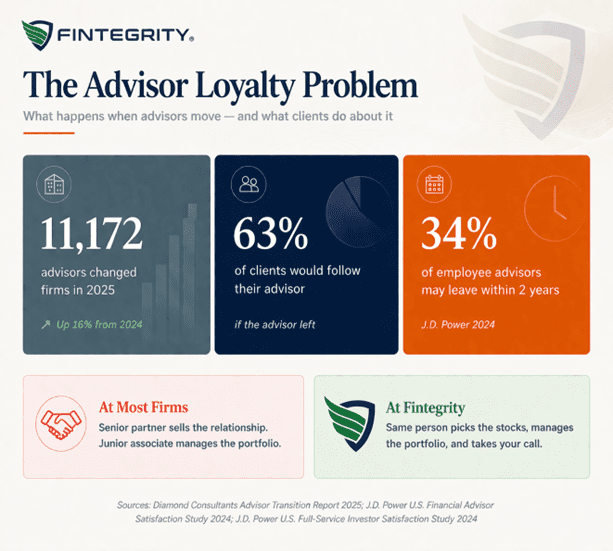

At most advisory firms, the business model depends on a division of labor. A senior advisor — often the person whose name is on the door — is responsible for business development (sales). They meet with prospective clients, establish the relationship, and close the engagement. Once you sign, your account enters a service model where the day-to-day management is delegated to associate advisors, portfolio analysts, or centralized investment teams.

This is not a secret. It is how virtually every wirehouse, large RIA, and multi-advisor practice operates. The economics require it. A senior advisor generating $2 million or more in annual revenue cannot personally manage 200 client relationships. The math does not work unless the work is distributed.

The problem is that the distribution often happens without a clear conversation about who will actually be making decisions for your portfolio. You hired a person. You received a team. And the person whose judgment persuaded you to sign may have little involvement in the ongoing management of your money.

Why Continuity of Decision-Maker Matters

This is not merely a customer service issue. The separation between the person who understands your situation and the person managing your portfolio creates tangible financial consequences.

Tax efficiency erodes. Effective tax management requires knowing your complete picture — not just what is in the portfolio, but your income trajectory, your charitable intentions, your estate plan, the cost basis of every position, and the timing of anticipated liquidity events. When one person holds all of that context and makes the investment decisions accordingly, tax-loss harvesting, gain deferral, and asset location can be coordinated precisely. When the person trading the account is working from a model portfolio with limited visibility into your tax situation, opportunities are missed. Tax drag — the silent reduction in after-tax returns — can cost 1% to 2% annually, and it compounds. Over 20 years on a $3 million portfolio, that is the difference between $9.6 million and $7.2 million. Not because of poor investment selection. Because of poor coordination.

Institutional knowledge disappears. Every client conversation reveals context that matters for future decisions. The reason you are overweight in a particular stock. The promise you made to your spouse about risk. The inheritance that is arriving next year. The concentrated position you cannot sell for sentimental or tax reasons. When the person managing the portfolio was not in those conversations, that context lives in a CRM note at best — and nowhere at worst. Decisions get made without it.

Risk tolerance becomes a form field. The senior advisor who sat across the table from you understood your risk tolerance through conversation, body language, and years of professional judgment. The associate who inherits your account understands it through a number on a questionnaire. These are not the same thing. When markets fall 20%, the person who knows you will manage through it differently than the person who knows your risk score.

Responsiveness declines. According to CEG Insights research, only 50.6% of high-net-worth clients agree that their advisor reaches out to them on a regular basis, and just 56.3% report having a high degree of trust in their advisor. Those numbers reflect a structural problem. When the person you trust is not the person managing your account, the relationship atrophies. You stop calling because you know you will not reach the person who understands your situation. The advisor stops calling because, in a team model, it is often unclear whose job that is.

The Industry’s Staffing Crisis Makes This Worse

The advisory industry is in the middle of a structural transformation that amplifies the handoff problem.

According to the Diamond Consultants Advisor Transition Report, 11,172 experienced advisors changed firms in 2025 — up 16% from the prior year. J.D. Power’s 2024 Financial Advisor Satisfaction Study found that 34% of employee advisors and 41% of independent advisors who are more than two years from retirement may leave their current firm within two years. McKinsey estimates that 110,000 advisors — 38% of the current workforce — will retire in the next decade, creating a shortage of 90,000 to 110,000 advisors by 2034.

What does this mean for you? If your portfolio is managed by a team rather than a specific person, the team will change. People will leave, retire, or be reassigned. Your account will be handed off again. J.D. Power found that 63% of investors would follow their advisor to a new firm if that advisor left. But if you do not have a specific advisor — if you have a team, a process, a service model — there is no one to follow. You simply start over with a new set of people who do not know your situation.

This is not a hypothetical. It is the default experience at most large advisory firms.

The Sole-Practitioner Model: A Feature, Not a Limitation

When prospective clients learn that Fintegrity® is a sole-practitioner firm, some wonder whether that is a limitation. It is a reasonable question. Let me explain why it is the opposite.

At Fintegrity, I am the person who researches and selects every stock and bond in your portfolio. I am the person who decides when to rebalance, when to harvest a tax loss, and when to hold through volatility. I am the person who answers the phone when you call and the person who calls you when something in the market warrants a conversation.

This means:

- Every investment decision carries the full context of your financial life. I know your tax situation because I manage around it every day. I know your risk tolerance because we discussed your preferences and I observed it through actual market cycles, not estimated it from a questionnaire. I know your estate plan because I read what you shared with me.

- There is no information loss between meetings. The person you spoke with in January is the same person adjusting your portfolio in June. Nothing falls through the cracks of a handoff memo or a CRM note that no one reads.

- Accountability is absolute. When there is one decision-maker, there is no ambiguity about who is responsible for the outcome. I cannot attribute a mistake to a model portfolio, a trading desk, or an associate who misunderstood the instruction. The decisions are mine, and I stand behind them.

- The relationship deepens rather than resets. Over years of working together, I develop an understanding of your family, your goals, and your temperament that no onboarding process can replicate. That understanding makes every subsequent decision better informed.

I serve approximately 24 families. That number is deliberate. It allows me to provide the kind of attention and customization that a 200-client practice structurally cannot, while maintaining the institutional-grade investment expertise that comes from three decades of professional portfolio management, including overseeing $40 billion in assets at TIAA.

What to Ask Before You Hire Anyone

Whether you choose Fintegrity or another firm, ask these questions before you sign:

“Who will actually manage my portfolio day to day?” If the answer is anyone other than the person sitting across from you, ask to meet that person. Evaluate their experience, their investment process, and their understanding of your situation.

“What happens if my advisor leaves the firm?” A clear succession plan matters. But at a firm where the senior advisor was never managing your money in the first place, the question is moot — you have already been handed off.

“How many clients does my advisor personally manage?” There is an upper bound on the number of relationships one person can serve with genuine attention. If your advisor manages 300 households, the attention you receive will reflect that ratio.

“Can I call my advisor directly when markets are volatile?” During the weeks when your portfolio drops 15%, you should be able to reach the person making decisions — not leave a message with a service team.

The Cost You Cannot See on a Statement

The hidden cost of being handed off never appears on a quarterly performance report. There is no line item for “lost tax efficiency due to team turnover” or “suboptimal decision because the associate did not know your full situation.” These costs accumulate silently, compounding over years, and they are real.

The advisory industry has built an infrastructure optimized for scale. That infrastructure works well for the firms. The question is whether it works well for you.

Jeffrey Barnett is the founder and Managing Principal of Fintegrity LLC, a registered investment adviser based in Tenafly, New Jersey. Fintegrity manages portfolios for approximately 20 high-net-worth families nationwide using individual stocks and bonds, with full discretionary authority. For more information, contact Jeff@Fintegrity.com or 201-266-6829.

Fintegrity is registered with the New Jersey Bureau of Securities. This article is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. All investments involve risk, including possible loss of principal.