January 24, 2026

By Jeffrey Barnett, Founder and Managing Principal, Fintegrity® LLC

Gold, silver, and other precious metals rallied over the past two years, capturing investor attention. Gold recently surpassed $4,700 per ounce while silver now trades above $90 per ounce, marking historic milestones for both metals. This strong recent performance may lead some investors to wonder whether they should be investing in these assets.

While many investors often turn to precious metals as “safe haven” investments, these and other commodities are prone to boom-and-bust cycles. In today’s environment, the rallies in gold and silver are occurring alongside many other asset classes due to heightened uncertainty around monetary policy, fiscal policy, and geopolitical risk.

Several factors have driven the surge in gold and silver prices. One of the most important has been the recent tension between the White House and the Fed. This has raised questions about central bank independence and the direction of monetary policy, especially as Jerome Powell’s term as Fed chair ends in May 2026. Lower rates and the prospect of inflation put downward pressure on the dollar, so it’s natural for some investors to seek assets that can serve as a “store of value.”

Equally important is that central banks around the world have been consistent buyers of gold in recent years as they have diversified away from dollar-denominated reserves. Central banks need to hold enough reserves to manage their monetary policy and maintain the value of their currencies. These purchases of gold and other assets have accelerated amid heightened geopolitical uncertainty and concerns about currency stability.

Both metals have also benefited from their industrial applications, including in electric vehicles, solar panels, and artificial intelligence hardware. Thus, they serve roles as precious metals, safe haven assets, as well as industrial commodities.

Throughout history, periods of monetary policy uncertainty have coincided with strong precious metals performance. In the 1970s, for instance, both gold and silver climbed dramatically as stagflation hit the economy, peaking around 1980. Similarly, both rose from 2008 to 2011 during the global financial crisis, and then again during the 2020 pandemic.

In each of these cases, investors turned to precious metals when uncertainty about monetary policy and economic conditions peaked. However, both gold and silver prices began to reverse soon after conditions began to improve.

This creates at least two challenges for investors who are attracted to these investments based on recent performance. First, attempting to forecast gold and silver prices amounts to predicting the path of interest rates, inflation, and other factors like terms of trade. As the past several years have shown, these factors are difficult to forecast with certainty. Many concerns among investors and professional economists as inflation spiked in 2021 and 2022 did not materialize as expected.

Second, while it’s understandable that investors are drawn to assets that have performed well, history shows that precious metal rallies are notoriously difficult to time. The 1970s gold rally, for instance, was followed by two decades of declining prices. Gold peaked above $800 in 1980, a level it wouldn’t reach again until 2007.

The accompanying chart shows gold’s performance compared to the S&P 500 since the 2007 market peak. While gold has had periods of strong performance, the stock market has also performed well over these periods. For investors focused on recent precious metals rallies, this longer-term perspective may seem surprising. However, it makes sense since the stock market has historically risen over long periods of time.

This pattern extends to silver as well. Despite its strong industrial demand story, silver has experienced long periods of underperformance between rallies. For instance, silver experienced a strong rally in the late 1970s. As stagflation pushed silver higher, a famous episode occurred in which the Hunt brothers attempted to corner the market by accumulating stockpiles and buying futures contracts. While they drove prices higher for a time, prices eventually plummeted as new supply entered the market and when regulators introduced restrictions on leveraged buying of commodities.

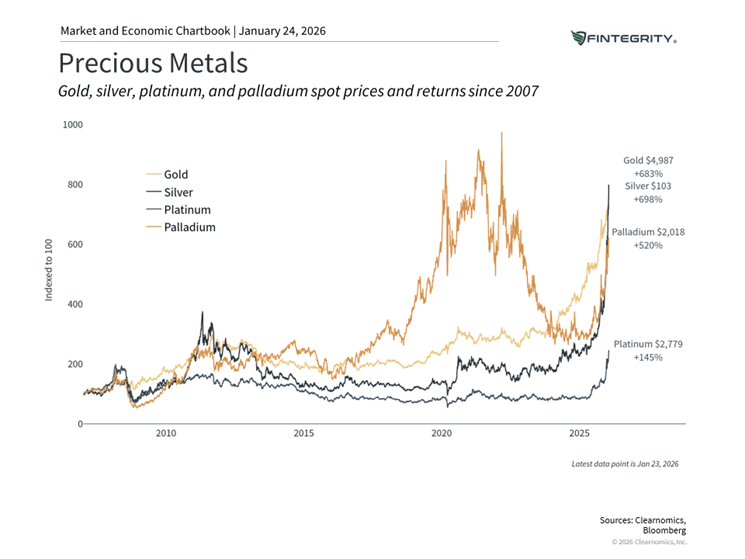

Other precious metals exhibit similar behavior. Between 2016 and early 2022, palladium gained over 500%. This rally was driven by restricted global supply and greater use in applications such as catalytic converters for cars. However, after peaking, prices declined sharply over a two-year period.

As the previous chart illustrates, commodities have largely underperformed since 2011, outpacing the stock market in only two of the past sixteen years.

For the majority of investors, a commodity allocation should remain a peripheral component of a broader strategy, if included at all. Within a modest commodity sleeve, the Bloomberg Commodity Index offers a helpful benchmark, currently weighting gold at 14.9% and silver at 3.9% alongside energy, agriculture, and industrial metals. Integrating precious metals into such a diversified basket can help temper the volatility inherent in any single commodity.

The argument for including precious metals hinges on their distinct behavior relative to traditional stocks and bonds. Their value is rooted in scarcity, a historical legacy as a store of value, and various industrial uses. Because these assets often respond to economic shifts independently of traditional markets, they can offer a stabilizing effect that bolsters portfolio resilience. This serves investors well when the primary goal is preserving purchasing power over long horizons, though it is less effective for those focused on wealth accumulation.

However, precious metals possess significant limitations. Unlike bonds or dividend-yielding stocks, they generate no income, which makes them notoriously difficult to value. This lack of cash flow also leaves them susceptible to speculative cycles of boom and bust. A portfolio too heavily concentrated in gold and silver risks forfeiting the long-term growth of equities and the reliable yield of fixed income assets. While beneficial under specific market conditions, they rarely align with primary long-term financial objectives.

Ultimately, gold and silver can serve as stabilizing agents during periods of market turbulence. Yet, given the recent surge in gold prices, the potential for downside risk has increased. A prudent approach would be to limit gold exposure to 5% or less of a total portfolio, keeping in mind that the current bull run is unlikely to persist indefinitely

Disclosures: Investing involves risk, including the potential loss of principal. Past performance does not guarantee future results. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and other information provided are subject to change without notice. This report does not consider the specific investment objectives, financial situation, or particular needs of any specific recipient.

Gold and Silver: Current Portfolio Perspectives

January 24, 2026

By Jeffrey Barnett, Founder and Managing Principal, Fintegrity® LLC

Gold, silver, and other precious metals rallied over the past two years, capturing investor attention. Gold recently surpassed $4,700 per ounce while silver now trades above $90 per ounce, marking historic milestones for both metals. This strong recent performance may lead some investors to wonder whether they should be investing in these assets.

While many investors often turn to precious metals as “safe haven” investments, these and other commodities are prone to boom-and-bust cycles. In today’s environment, the rallies in gold and silver are occurring alongside many other asset classes due to heightened uncertainty around monetary policy, fiscal policy, and geopolitical risk.

Several factors have driven the surge in gold and silver prices. One of the most important has been the recent tension between the White House and the Fed. This has raised questions about central bank independence and the direction of monetary policy, especially as Jerome Powell’s term as Fed chair ends in May 2026. Lower rates and the prospect of inflation put downward pressure on the dollar, so it’s natural for some investors to seek assets that can serve as a “store of value.”

Equally important is that central banks around the world have been consistent buyers of gold in recent years as they have diversified away from dollar-denominated reserves. Central banks need to hold enough reserves to manage their monetary policy and maintain the value of their currencies. These purchases of gold and other assets have accelerated amid heightened geopolitical uncertainty and concerns about currency stability.

Both metals have also benefited from their industrial applications, including in electric vehicles, solar panels, and artificial intelligence hardware. Thus, they serve roles as precious metals, safe haven assets, as well as industrial commodities.

Throughout history, periods of monetary policy uncertainty have coincided with strong precious metals performance. In the 1970s, for instance, both gold and silver climbed dramatically as stagflation hit the economy, peaking around 1980. Similarly, both rose from 2008 to 2011 during the global financial crisis, and then again during the 2020 pandemic.

In each of these cases, investors turned to precious metals when uncertainty about monetary policy and economic conditions peaked. However, both gold and silver prices began to reverse soon after conditions began to improve.

This creates at least two challenges for investors who are attracted to these investments based on recent performance. First, attempting to forecast gold and silver prices amounts to predicting the path of interest rates, inflation, and other factors like terms of trade. As the past several years have shown, these factors are difficult to forecast with certainty. Many concerns among investors and professional economists as inflation spiked in 2021 and 2022 did not materialize as expected.

Second, while it’s understandable that investors are drawn to assets that have performed well, history shows that precious metal rallies are notoriously difficult to time. The 1970s gold rally, for instance, was followed by two decades of declining prices. Gold peaked above $800 in 1980, a level it wouldn’t reach again until 2007.

The accompanying chart shows gold’s performance compared to the S&P 500 since the 2007 market peak. While gold has had periods of strong performance, the stock market has also performed well over these periods. For investors focused on recent precious metals rallies, this longer-term perspective may seem surprising. However, it makes sense since the stock market has historically risen over long periods of time.

This pattern extends to silver as well. Despite its strong industrial demand story, silver has experienced long periods of underperformance between rallies. For instance, silver experienced a strong rally in the late 1970s. As stagflation pushed silver higher, a famous episode occurred in which the Hunt brothers attempted to corner the market by accumulating stockpiles and buying futures contracts. While they drove prices higher for a time, prices eventually plummeted as new supply entered the market and when regulators introduced restrictions on leveraged buying of commodities.

Other precious metals exhibit similar behavior. Between 2016 and early 2022, palladium gained over 500%. This rally was driven by restricted global supply and greater use in applications such as catalytic converters for cars. However, after peaking, prices declined sharply over a two-year period.

As the previous chart illustrates, commodities have largely underperformed since 2011, outpacing the stock market in only two of the past sixteen years.

For the majority of investors, a commodity allocation should remain a peripheral component of a broader strategy, if included at all. Within a modest commodity sleeve, the Bloomberg Commodity Index offers a helpful benchmark, currently weighting gold at 14.9% and silver at 3.9% alongside energy, agriculture, and industrial metals. Integrating precious metals into such a diversified basket can help temper the volatility inherent in any single commodity.

The argument for including precious metals hinges on their distinct behavior relative to traditional stocks and bonds. Their value is rooted in scarcity, a historical legacy as a store of value, and various industrial uses. Because these assets often respond to economic shifts independently of traditional markets, they can offer a stabilizing effect that bolsters portfolio resilience. This serves investors well when the primary goal is preserving purchasing power over long horizons, though it is less effective for those focused on wealth accumulation.

However, precious metals possess significant limitations. Unlike bonds or dividend-yielding stocks, they generate no income, which makes them notoriously difficult to value. This lack of cash flow also leaves them susceptible to speculative cycles of boom and bust. A portfolio too heavily concentrated in gold and silver risks forfeiting the long-term growth of equities and the reliable yield of fixed income assets. While beneficial under specific market conditions, they rarely align with primary long-term financial objectives.

Ultimately, gold and silver can serve as stabilizing agents during periods of market turbulence. Yet, given the recent surge in gold prices, the potential for downside risk has increased. A prudent approach would be to limit gold exposure to 5% or less of a total portfolio, keeping in mind that the current bull run is unlikely to persist indefinitely

Disclosures: Investing involves risk, including the potential loss of principal. Past performance does not guarantee future results. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and other information provided are subject to change without notice. This report does not consider the specific investment objectives, financial situation, or particular needs of any specific recipient.

Speak with Our Investment Strategist in Fairfield About Your Portfolio.