By Jeffrey Barnett, Founder and Managing Principal, Fintegrity LLC

For long-term investors, understanding what can and cannot be controlled is crucial for financial success and peace of mind. While every investor may want to predict market movements, experience teaches us that it is a challenging task.

The Optimal Approach

The optimal approach involves constructing and managing a suitable portfolio, making strategic and tactical allocations based on market opportunities, ideally with assistance from a trusted advisor. Success is more likely by saving early, staying invested, and remaining focused on long-term financial goals.

Maintaining financial discipline is more important than ever, given the surge of information from media and the financial services industry. Headlines seem to jump from one concern to the next every week, causing markets to swing between exuberance and distress.

Lessons from History

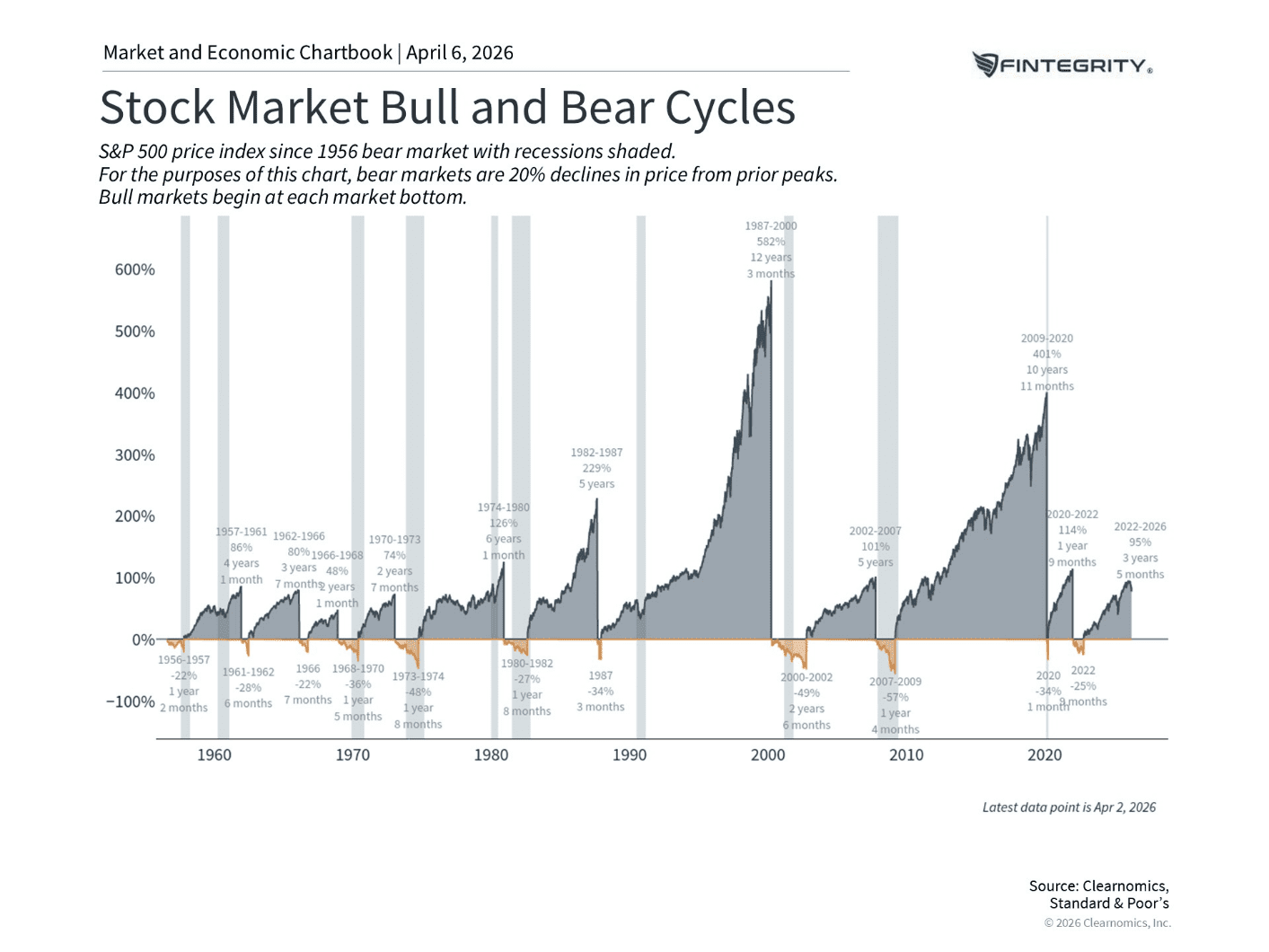

This is not a new phenomenon. In 1979, BusinessWeek famously declared “the death of equities” due to inflation — a sentiment echoed by many investors in subsequent decades during periods of economic uncertainty. In the short term, these assessments seemed correct, as markets retraced due to economic shocks and recessions. Yet, both the market and the economy ultimately recovered.

The subsequent four-plus decades since that magazine cover was published have been some of the most fruitful in market history, reinforcing a fundamental truth: pessimism may sell headlines, but optimism has rewarded patient investors.

A Century of Evidence

This pattern holds when we look further back in time. A single dollar invested in the S&P 500 in 1926 — with dividends reinvested — would have grown to approximately $20,000 by the end of 2025. That is a century of compounding through depressions, world wars, oil crises, financial panics, and pandemics.

By comparison, the same dollar invested in government bonds would have grown to roughly $100, and inflation over the same period means that approximately $17 is now required to purchase what $1 bought in 1926. The gap between stocks and every other asset class is not a matter of a few percentage points — it is orders of magnitude.

These figures demonstrate the significant wealth generated by the stock market for patient investors. Bonds remain a necessary component of a well-constructed portfolio to mitigate volatility, but the long-term case for equities is compelling.

The Power of Starting Early

Equally important is the timing of saving and investment. Consider a starting investment of $1,000, compounding annually at 7%. Invested at the age of 30, that sum could potentially grow to over $10,000 by age 65. If the same investment is made at age 35 — just five years later — it would reach only approximately $7,600. Those five years account for roughly a quarter of the total outcome, illustrating why early action matters so much.

Staying the Course

Invest early and remain committed, even during challenging times. History shows this is the most effective strategy for realizing long-term financial objectives.

Disclosures

This article is for informational purposes only and does not constitute investment advice. All investments involve risk, including possible loss of principal. Past performance does not guarantee future results. Fintegrity LLC is a registered investment adviser regulated by the New Jersey Bureau of Securities.